Payment Processors vs Settlement Ledgers: Why They Are Not the Same

A category-definition article explaining how payment processors and settlement ledgers work together in governed payout workflows.

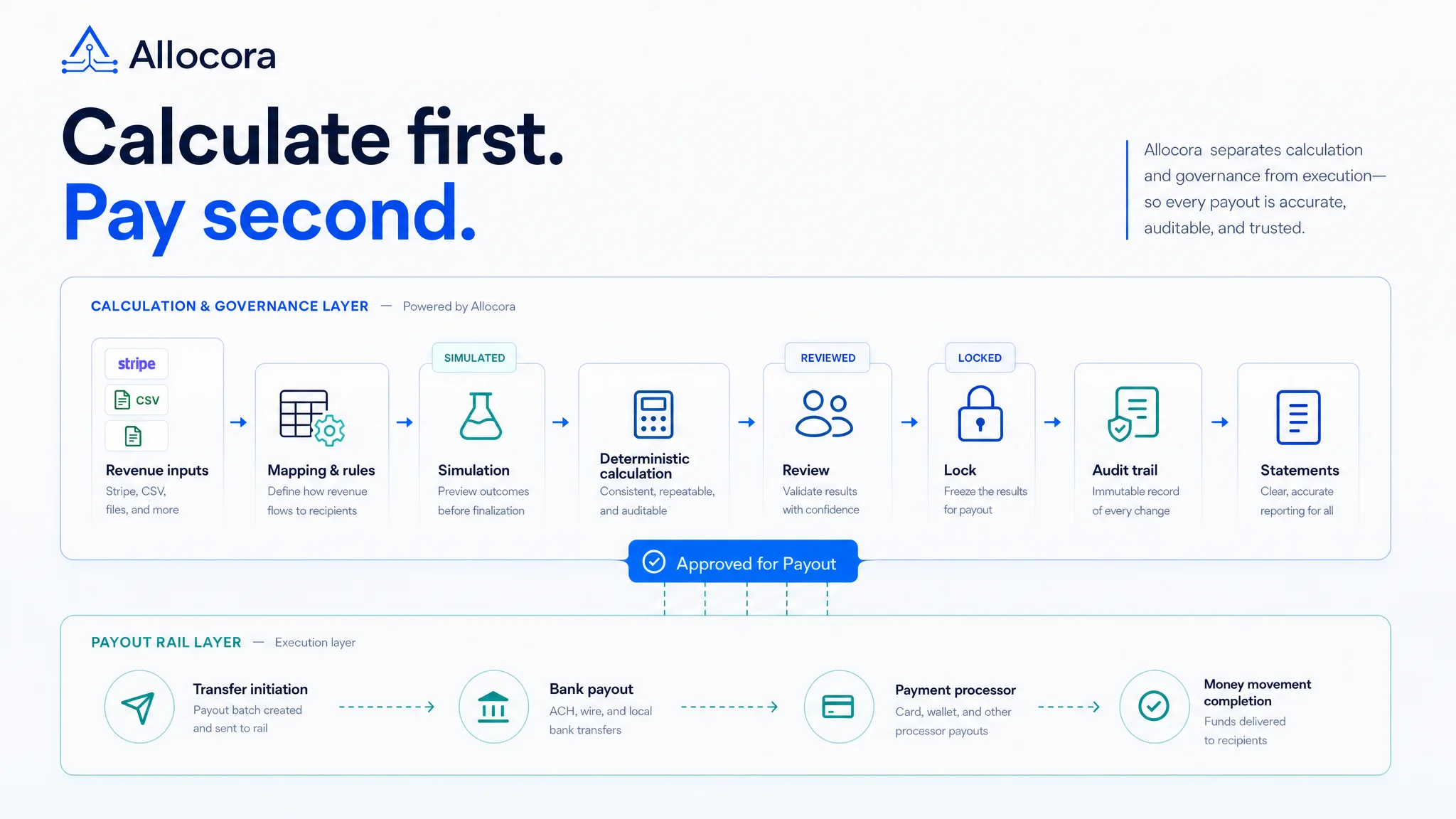

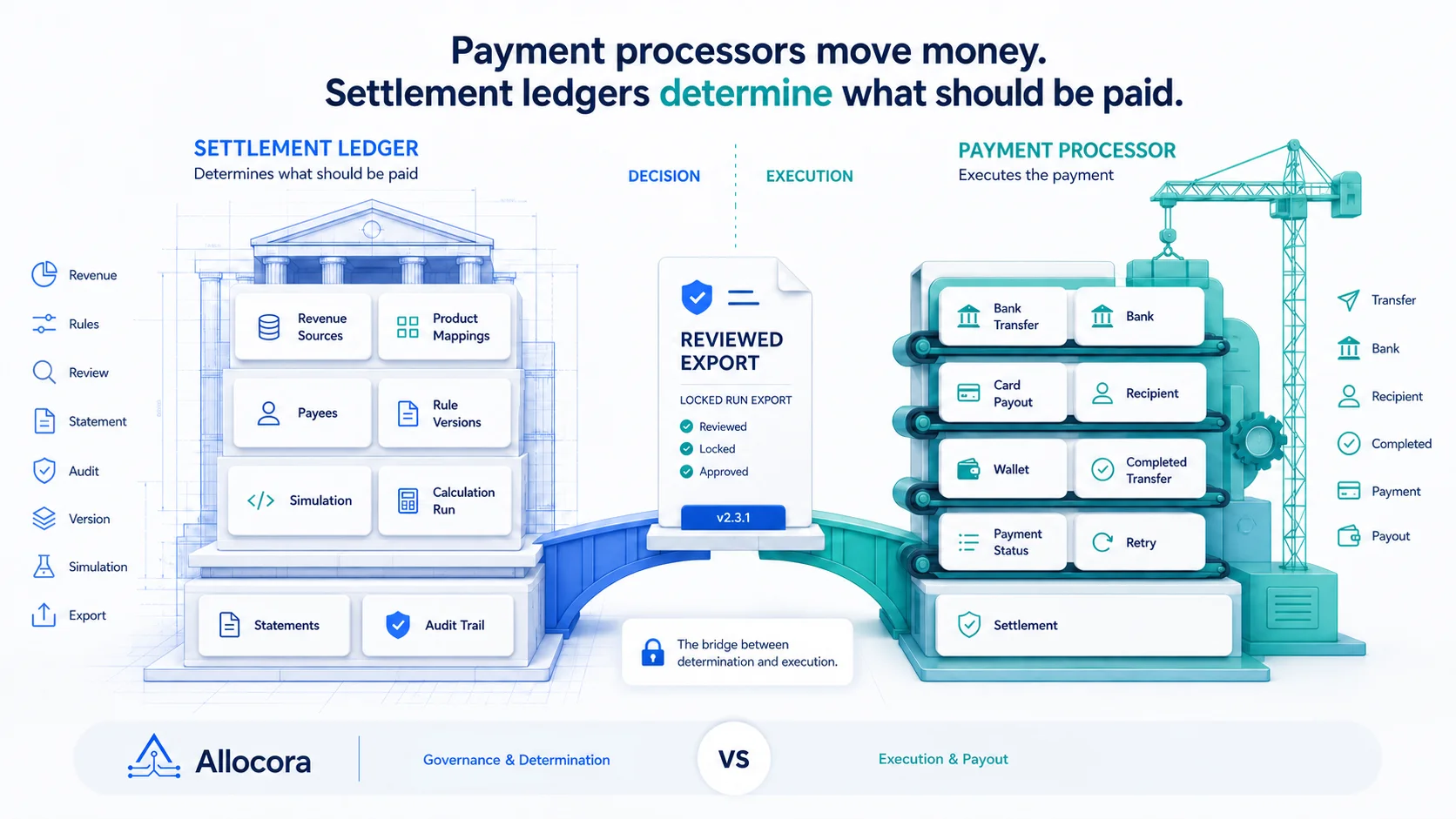

Payment processors and settlement ledgers solve different jobs. A payment processor helps move money. A settlement ledger helps determine what should be paid, why it should be paid, and what evidence supports that amount before payment execution.

Teams often confuse the two categories because both sit near payout workflows. A marketplace may use Stripe Connect to pay sellers. A SaaS company may use a bank transfer workflow for partners. An agency may pay contractors through accounting software. Those systems can move funds, but they usually do not own every rule, version, calculation, statement, export, and audit event required to explain complex revenue allocation.

Allocora fits the settlement ledger side of the workflow. It calculates and governs payouts from revenue data, creates deterministic calculation runs, preserves immutable snapshots, generates statements, and exports structured files. It does not move money, perform KYC/AML, collect tax forms, or replace the payment processor.

This article explains the distinction and why teams with complex payout logic often need both.

What payment processors do

Payment processors and payout rails handle execution. Depending on the provider, they may support:

- Account onboarding.

- Identity verification.

- Compliance workflows.

- Bank payouts.

- Card payouts.

- Wallets.

- Transfer scheduling.

- Retry logic.

- Reporting on transferred funds.

- Recipient payment status.

These are essential capabilities. If a business needs to send money at scale, it needs a reliable payment execution layer.

But money movement is not the same as payout calculation. A payment processor can send $12,400 to a partner. It may not explain why that partner earned $12,400, which revenue rows were included, which rule version applied, or how a refund changed the amount.

That is the settlement ledger problem.

What settlement ledgers do

A settlement ledger handles calculation and evidence before money moves. It should connect:

- Source revenue.

- Products or external identifiers.

- Payees.

- Rules.

- Refunds.

- Adjustments.

- Calculation runs.

- Statements.

- Exports.

- Audit logs.

The settlement ledger is where the organization decides the expected payout. The payment processor is where the organization executes it.

We covered this distinction from another angle in Payout Rails vs Payout Calculation Software: Why Teams Need Both.

Allocora's current product surface includes Stripe and file-based revenue ingestion, product mapping, payees, rules, rule simulation, deterministic calculation runs, statements, structured exports, and audit logs. That makes it a settlement calculation and governance layer rather than a payment execution tool.

Why calculation should happen before payout execution

The safest payout workflow reviews the calculation before any transfer is triggered.

If calculation happens inside a spreadsheet, the team may have formula drift, hidden edits, inconsistent statement creation, and weak audit history. If calculation happens only inside a payment processor, the team may lack a flexible place to model business-specific rules and preserve payout evidence.

Before payment execution, finance and operations should be able to answer:

- Which revenue rows are included?

- Which payees are eligible?

- Which products are mapped?

- Which rules apply?

- Are refunds and adjustments handled explicitly?

- Were rule conflicts resolved?

- Has the run been reviewed or locked?

- Do statements match the calculated totals?

- Is the export ready for the downstream rail?

Those questions belong in the settlement ledger.

Examples of rules payment tools usually do not own

Payment processors are not designed to own every settlement rule a business can invent.

Examples include:

- A SaaS partner receives 10 percent recurring revenue on one product and 15 percent after a threshold.

- A marketplace seller has a platform fee that varies by category and tier.

- An agency contractor receives a share only after a milestone payment is received.

- A royalty-style payee receives a split after deductions and adjustments.

- A partner rule applies only to a source, territory, or metadata condition.

- A refund should claw back a prior payout in the current period.

These are business rules. They need versioning, simulation, review, and historical traceability.

Allocora supports flat and tiered rules, metadata conditions, effective windows, priority handling, rule conflict checks, and immutable rule versions. That gives teams a controlled place to manage payout logic before exporting results to a payment workflow.

Why spreadsheets are not a durable settlement ledger

Many teams use spreadsheets as their settlement ledger. This is understandable. Spreadsheets are fast, flexible, and familiar. They are useful for early modeling and ad-hoc analysis.

They become weak as settlement infrastructure because they usually lack:

- Immutable source facts.

- Versioned payee records.

- Versioned rule records.

- Conflict detection.

- Deterministic run snapshots.

- Statement generation tied to the run.

- Audit logs across changes.

- Repeatable export workflows.

A workbook can calculate. It rarely governs.

We explored that transition in Replace Spreadsheet Commission Tracking Before Month-End Breaks.

That difference matters when a partner, seller, contractor, or auditor asks how a payout was calculated.

Where Allocora sits in the stack

A clean payout stack can look like this:

- Source systems produce revenue data.

- Allocora imports or normalizes that revenue.

- Allocora maps products and payees.

- Allocora applies versioned settlement rules.

- Allocora creates a deterministic calculation run.

- Finance reviews the run and generated statements.

- Allocora exports payout-ready files or close packages.

- A payment processor or finance workflow executes payment.

This makes Allocora the calculation and evidence layer between source revenue and payment execution.

It also keeps the categories honest. Allocora does not replace Stripe Connect, bank transfers, or payment operations. It prepares reviewed amounts for those workflows.

What an audit-ready settlement ledger should include

An audit-ready settlement ledger should include more than a balance table.

It should preserve:

- Source data traceability.

- Product and payee mapping context.

- Rule version history.

- Calculation run snapshots.

- Line-level calculation output.

- Statement generation events.

- Export records.

- Audit logs for key changes.

Allocora's current implementation supports these areas across revenue sources, revenue imports, products and mappings, payees, rules, calculation runs, statements, exports, integrations, and audit logs.

That breadth matters because payout errors can originate anywhere in the workflow.

How settlement ledgers reduce payout disputes

Disputes often happen when a payee sees only a final number. A settlement ledger reduces disputes by making the calculation explainable.

For example, a partner statement can show the period, products, revenue, deductions, rule context, and amount owed. If the payee asks a follow-up question, the team can trace back to the run and source data instead of reconstructing a spreadsheet.

The strongest dispute workflow is not reactive. It produces clear statements and audit-ready exports as part of the normal close process.

Audit-ready review processes are also a core part of How Immutable Calculation Runs Create a Payout Audit Trail.

Allocora's statement generation from locked calculation runs supports that pattern.

The handoff artifact matters

The handoff between a settlement ledger and a payment processor should be an artifact, not a conversation. A person saying "the spreadsheet is ready" is not enough. The downstream payment workflow should receive reviewed totals, statement files, and enough supporting context to prove that the amounts were calculated from the approved run.

In Allocora, that handoff can be built from the calculation run and its exports. A reviewed run can produce payee totals, detailed calculation items, statement summaries, statement PDFs, and close packages. Those outputs become the practical bridge between calculation and payment execution.

This reduces operational ambiguity. The payment processor handles transfer execution. Allocora provides the reviewed amount and the evidence behind it.

The category boundary protects implementation choices

Clear category boundaries also protect product and implementation decisions. If a team expects a settlement ledger to become a payment processor, it may overbuild recipient onboarding, tax workflows, and funds movement before it has solved the calculation problem. If a team expects a payment processor to become a settlement ledger, it may hide business-specific payout rules in exports, scripts, or spreadsheets.

Allocora's boundary is intentionally narrower. It focuses on settlement calculations, statements, exports, audit history, and governance before payout execution. That makes it more practical for teams that already have a payment method but lack a reliable way to calculate what each payee should receive.

For buyers, the evaluation question should be precise: "Do we need help moving money, or do we need help proving the payout amount before money moves?" Many teams eventually need both, but they should not confuse them.

When a payment processor alone is enough

A payment processor alone may be enough when:

- Payout logic is simple.

- There are few payees.

- There is one source of revenue.

- The payment tool owns the complete calculation workflow.

- The team does not need detailed statements.

- There is little risk of future dispute or audit review.

In that case, adding a settlement ledger may be unnecessary.

When to add a settlement ledger

Add a settlement ledger when:

- Payout logic involves multiple payees or products.

- Rules change over time.

- Refunds and adjustments affect payout amounts.

- Payees need statements.

- Finance needs a close artifact.

- Payout files are currently assembled in spreadsheets.

- The team needs to prove how an amount was calculated.

These are the situations where teams typically outgrow spreadsheets and payout-only workflows.

Launch takeaway

Payment processors and settlement ledgers are not the same. Payment processors move money. Settlement ledgers calculate, explain, export, and audit payout amounts before money moves.

Allocora is a settlement ledger for rules-driven revenue allocation and payout calculations. It helps teams move from fragile spreadsheets to deterministic settlement runs while keeping their existing payment processor or payout rail.